Saving is an important task in order to achieve our long-term goals. However, it can be difficult and demotivating when we do not see immediate results. In this article, we present some tips on how to save effectively for your future projects.

Identify your goals

The first thing you should do is define what you want to achieve in the long term: do you want to buy a house, travel the world, save for your children's education or simply have an emergency fund?

It is important that you know how much money you will need to achieve each of these goals and how long you want to achieve them. This way, you will be able to establish a realistic and achievable savings plan.

Establish a budget

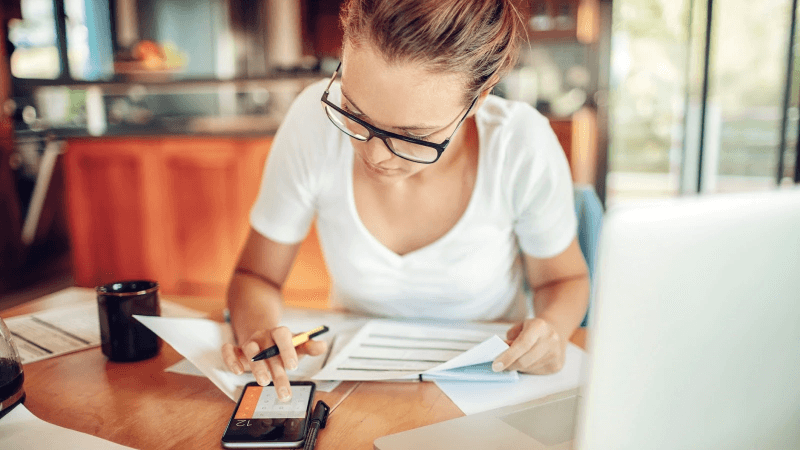

The first step in saving for your long-term goals is to establish a clear budget that allows you to manage your income and expenses effectively. To do this, it is important to write down all your daily, monthly and annual expenses to have a clear idea of how much money you need to cover your basic needs and how much you have left over to save.

Once you have a budget in place, you can identify areas where you can reduce expenses, such as eating out or unnecessary purchases. With the money saved, you can allocate a portion to your long-term goals.

It is also important to set clear and realistic goals for your savings so that you know how much money you need to save each month to reach them by the deadline. Also, if you have difficulty managing your budget, there are online tools and applications that can help you keep track of your income and expenses more efficiently. Don't miss the opportunity to start saving today!

Reduce unnecessary expenses

One of the best ways to save money is to reduce unnecessary expenses. This means analyzing your spending habits and determining where you are spending more than you should. You can start by making a detailed list of your monthly expenses and categorizing them into "necessary" and "unnecessary". Then, identify those expenses that you can reduce or eliminate altogether.

For example, if you eat out frequently, you could reduce this expense by cooking more at home. Or if you have subscriptions to services you don't use regularly, cancel those subscriptions to save money. Reducing unnecessary expenses may be difficult at first, but in the long run it will help you have more money available to save and reach your financial goals.

Increase your income

An effective way to save for your long-term goals is to increase your income. This can be through an increase in your current salary or by seeking alternative sources of income.

There are different ways to increase your income, such as working overtime, looking for an additional part-time job, selling products or services online, or freelancing. You can also consider improving your skills and education to qualify for a better salary and promotion in your current job. Remember that increasing your income should not be an excuse to spend more, but a strategy to reach your long-term financial goals.

Automate your savings

An effective way to save for your long-term goals is to automate your savings. This means that you set an amount of money to save each month and the transfer is automatically made from your checking account to your savings account.

By automating your savings, you ensure that you won't forget to do it and you won't have to worry about manually transferring the money each month. It will also help you to be disciplined about your spending, since you will have a clear and defined budget.

Also, if you have a job with regular income, consider setting up an automatic transfer directly from your payroll account to your savings account to make the process even easier. Remember, the easier it is to save, the more likely you are to be successful.

Look for investment opportunities

Once you've reached your short-term savings goals, it's important to start thinking about investing your money to increase its value. There are many investment options available, from stocks and bonds to real estate and mutual funds.

It is important to carefully research each option and choose the one that best suits your financial needs and goals. It is also advisable to seek expert financial advice before making any investment decisions. Remember that investing involves risk and does not guarantee returns, so it is important to have a clear strategy and be willing to take the risks necessary to achieve your long-term financial goals.

Be consistent and disciplined

Last but not least, it is essential to be consistent and disciplined in the savings process to achieve our long-term goals. This involves setting a realistic budget, sticking to it and avoiding spending on unnecessary things. It is also important to keep reviewing and adjusting the savings plan if necessary. Consistency and discipline will allow us to reach our goals faster and with less effort.